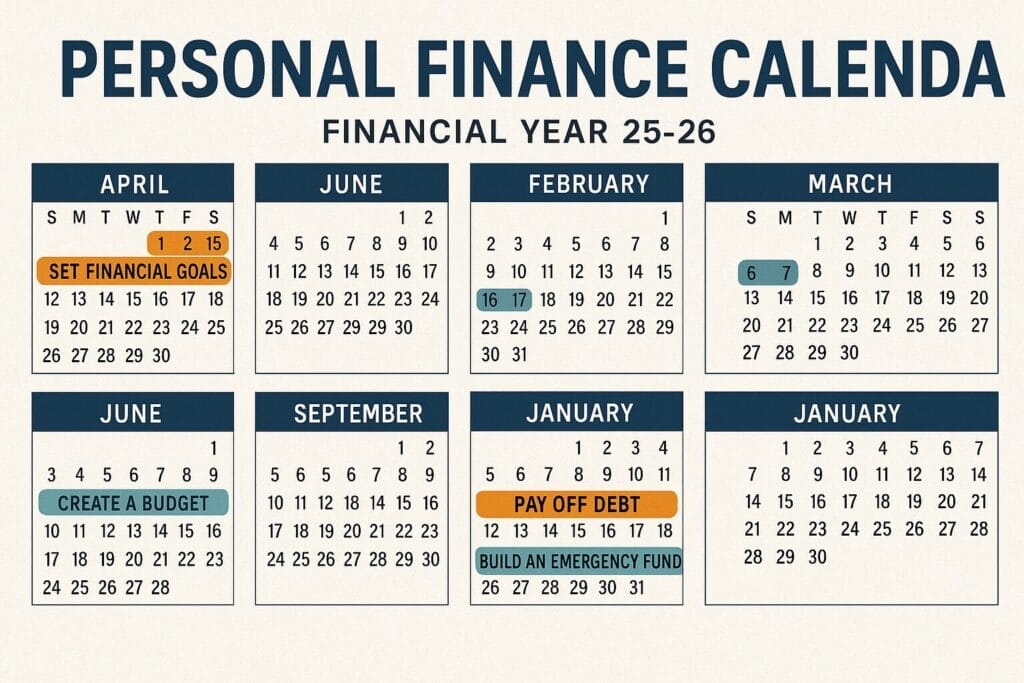

Financial Planning for Business Owners: How to Manage Personal & Business Wealth Managing finances as a business owner can be a complex balancing act, particularly when personal and business expenses often intertwine. Understanding how to separate these finances is crucial for achieving financial stability and maximising growth. This article outlines essential strategies for creating budgets, setting financial goals, and planning for savings and retirement, while emphasising the importance of seeking professional advice and implementing smart tax strategies. Whether you aim to avoid common pitfalls or prepare for future growth, these insights will enable you to navigate your financial landscape with confidence. 1. Understanding the Importance of Separating Personal and Business Finances Separating personal and business finances is fundamental to effective financial planning for you as a business owner. This practice not only simplifies your financial management but also provides you with a clearer view of your personal assets and business profitability. By maintaining this separation, you can achieve accurate budgeting techniques and effective cash flow management, leading to better financial decision-making, wealth accumulation, and ultimately enhancing your financial independence. When your finances are properly categorised, you can conduct financial health checks more effectively and make informed decisions regarding investments, liabilities, and tax obligations, all of which are crucial for long-term success and compliance with financial regulations and taxation strategies. For example, mixing personal and business finances can lead to unintended overspending and mismanagement of resources, potentially causing cash flow issues that could hinder your growth. In terms of tax planning strategies, combining these expenses may result in missed deductions or even reclassification by tax authorities, which could lead to costly penalties and affect your financial sustainability. Maintaining distinct accounts helps establish your credibility and provides a solid financial foundation, particularly when seeking loans or attracting investors. By keeping these areas separate, you can enjoy streamlined operations, reduced stress, and a clearer pathway to achieving your financial goals. 2. Creating a Budget for Personal and Business Expenses Creating a budget for both personal and business expenses is a fundamental aspect of effective financial planning that allows you to manage cash flow projections and achieve your financial goals and revenue streams. To begin this budgeting process, you should identify all sources of income and categorise your expenses into fixed and variable. This classification helps you understand where the majority of your funds are allocated and where you can make cuts if necessary. Utilising expense tracking apps can greatly simplify this process, offering valuable insights into your spending habits and patterns, which are crucial for liquidity and financial statement analysis. Maintaining a cash management strategy is crucial, ensuring that funds are available when needed and helping to prevent overspending. Regularly reviewing your budget is essential, as it enables you to make adjustments in response to changes in your financial circumstances or goals. Financial tools, such as online budgeting software, can automate calculations and provide visual reports, ultimately streamlining the budgeting process and enhancing its efficiency. 3. Setting Financial Goals for Both Personal and Business Finances Setting clear financial goals for both personal and business finances is essential for achieving long-term financial stability, business planning, and success. These goals serve as a roadmap for you as a business owner navigating your financial journey. Establishing these goals involves understanding and differentiating between short-term objectives, such as managing daily expenses or preparing for upcoming purchases, and long-term ambitions, including retirement planning or business expansion. Effective financial planning requires careful consideration of these goals to ensure they align with your overall vision. By tracking progress towards these objectives using relevant financial metrics, you can evaluate your strategies, adapt to changes in circumstances, and reinforce your commitment to comprehensive wealth management. This proactive approach enables you to make informed decisions that directly correlate with your objectives. 4. Creating a Plan for Savings and Investments Developing a comprehensive plan for savings, investment strategies, and investments is essential for business owners aiming to secure their financial future and achieve their financial goals while maximising wealth accumulation and shareholder equity. To create a successful savings strategy, you should first assess your current financial situation, including income, expenses, and debts. This initial evaluation serves as the foundation for setting realistic financial goals, whether they are short-term or long-term. Once you establish these objectives, you can explore various investment vehicles, such as shares, bonds, and unit trusts, each carrying its own risk and return profile. Understanding asset allocation principles is crucial at this stage, as it helps you determine how to distribute your investments across different asset classes to minimise risk. Incorporating a diversified investment portfolio not only protects you against market volatility but also enhances the potential for favourable returns over time. 5. Managing Debt for Both Personal and Business Finances Effective debt management is essential for maintaining financial stability, managing your credit management, and ensuring healthy cash flow in both personal and business finances. It enables you to navigate your financial obligations while ensuring healthy cash flow. This process involves implementing several strategies, such as consolidating loans to simplify payments and potentially reduce interest rates, which can alleviate some of the financial burden. Prioritising payments based on interest rates and due dates is crucial to prevent late fees and further interest accumulation. Understanding the implications of different types of debt, including personal liabilities and various business loans, enables you to make informed decisions that protect your assets. By balancing debt levels with available cash flow, you can create an environment that not only accommodates regular expenses but also supports growth and investment opportunities. 6. Reviewing and Updating Insurance Coverage Regularly reviewing and updating your insurance coverage is essential for risk management and protecting both your personal and business assets. This ensures that you are adequately safeguarded against potential risks. By taking a proactive approach, you can identify any gaps in your policies, such as the need for liability insurance to shield against third-party claims or specialised asset protection plans that cover critical business resources. As your business grows or shifts