Should I work with a fee only financial Planner or DIY Financial Planning?

Making informed financial choices can be a daunting task for many individuals. There are various options available when it comes to managing your finances, including relying on a financial planner or doing it yourself. This dilemma has been a hot topic among people looking to invest their money and make better financial decisions. While both options have their advantages and disadvantages, it is essential to understand their unique characteristics before choosing what suits you best.

In this blog post, we will be discussing the question on many people’s minds: “Should I work with a fee only financial planner or DIY financial planning?” We will explore the benefits and drawbacks of each option, giving you a clear understanding of what to expect when working with a financial planner or doing it yourself. The post will also provide insights into how a fee only financial planner operates and how DIY financial planning works.

Whether you’re a seasoned investor or a novice, this post will serve as a comprehensive guide, helping you make an informed decision on what’s best for you.

1. Understanding the difference between fee-only and DIY financial planning.

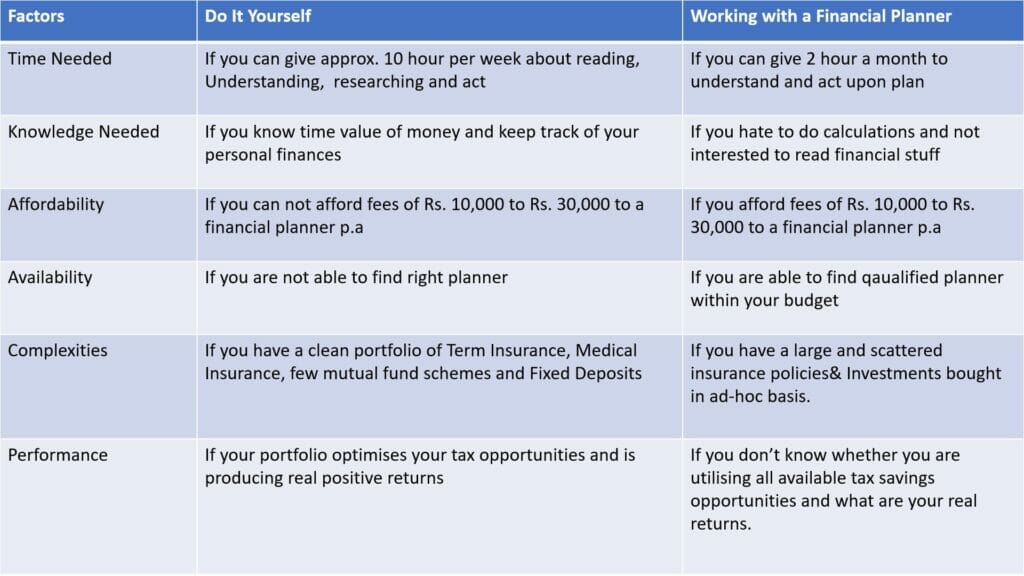

When it comes to financial planning, there are two main options: working with a fee-only financial planner or taking a DIY approach. Understanding the difference between these two options is essential in making an informed decision about which route to take. Fee-only financial planning involves working with a professional who is compensated only by the fees paid by clients, rather than receiving commissions for selling financial products. This approach ensures that the planner’s recommendations are not influenced by financial incentives to sell products. On the other hand, DIY financial planning involves managing your finances on your own, without the assistance of a professional. While this approach gives you more control over your finances, it may require more time and knowledge on your part, and you may miss out on potential benefits of working with a professional. Ultimately, the decision of whether to work with a fee-only financial planner or take a DIY approach depends on your individual financial situation and preferences.

2. Benefits of working with a fee-only financial planner.

If you’re considering working with a financial planner, it’s important to understand the different types of planners available. One option is a fee-only financial planner, who is compensated solely by the fees paid by clients and not through commissions or other incentives. One of the key benefits of working with a fee-only financial planner is that their advice is unbiased and not influenced by potential financial gains from recommending certain products. This allows them to act in the best interest of their clients and provide objective financial advice. Additionally, fee-only financial planners often have a fiduciary duty to their clients, meaning they are legally obligated to act in their clients’ best interests. This can provide peace of mind and confidence in the advice and recommendations provided by the planner. Overall, working with a fee-only financial planner can provide valuable benefits for those seeking objective financial advice and guidance.

Key Advantages of Fee-Only Financial Planning:

1. Professional expertise: Fee-only financial planners have specialized knowledge and expertise that can help you make informed decisions about your finances.

2. Objective perspective: Fee-only financial planners are trained to provide objective, unbiased advice that aligns with your financial goals.

3. Time-saving: Working with a fee-only financial planner can save you time and hassle, as the planner will handle the research, analysis, and decision-making.

3. DIY financial planning: Pros and cons.

DIY financial planning can be an attractive option for those looking to save money and take control of their finances. However, it is important to consider the pros and cons before committing to this approach. One advantage of DIY financial planning is the cost savings. By managing your own finances, you can avoid the fees associated with hiring a financial planner. Additionally, DIY financial planning allows you to have complete control over your investments and financial decisions. However, there are also potential downsides to this approach. Without the guidance of a professional financial planner, you may not have access to the most up-to-date information and strategies for maximizing your investments. Additionally, DIY financial planning can be time-consuming and may require a significant amount of research and education on your part. Ultimately, the decision to work with a fee-only financial planner or pursue DIY financial planning depends on your individual needs, goals, and comfort level with financial management.

4. What to consider before choosing DIY financial planning.

Before deciding to embark on DIY financial planning, there are several important factors to consider.

a. Solid understanding of basic financial principles: You must have knowledge of basics such as budgeting, saving, investing, and retirement planning. Without a strong foundation in these areas, it can be difficult to make informed decisions about your finances.

b. Willingness to invest significant time: You must be willing to invest significant time and effort into researching and implementing your financial plan. This may involve reading books, attending seminars, and monitoring market trends on a regular basis.

c. Being disciplined and organized: You must be disciplined and organized, as DIY financial planning requires a high level of self-motivation and accountability. d. Finally, it’s important to recognize that DIY financial planning carries certain risks, including the potential for making costly mistakes or overlooking important details.

As such, it’s crucial to weigh the pros and cons carefully before deciding whether to work with a fee-only financial planner or to pursue DIY financial planning.

5. What to look for in a fee-only financial planner.

If you are considering hiring a fee-only financial planner, it is important to know what to look for in order to ensure that you are getting the best possible service. Here are five key factors to consider:

1. Credentials: Look for a planner who holds certifications like Certified Financial Planner (CFP) or Chartered wealth management or Chartered Financial Analyst (CFA). These certifications demonstrate that the planner has undergone rigorous training and meets high ethical standards.

2. Experience: Look for a planner who has experience working with clients in situations similar to yours. Ask for references and check online reviews to get an idea of their track record.

3. Transparency: Fee-only financial planners charge a fee for their services, and do not earn commissions or kickbacks from selling financial products. Make sure your planner is transparent about their fees and any potential conflicts of interest.

4. Communication: A good financial planner should be able to explain complex financial concepts in terms you can understand, and should be responsive to your questions and concerns.

5. Approach: Look for a planner who takes a holistic approach to financial planning, taking into account your entire financial picture, including investments, debt, taxes, and estate planning. They should be able to create a customized plan that fits your unique

6. How fee-only financial planners are compensated.

Fee-only financial planners are compensated in a transparent way that ensures they act in the best interests of their clients. Instead of earning commissions for selling financial products, fee-only planners charge clients a flat fee or a percentage of assets under management for their services. This compensation structure eliminates potential conflicts of interest and incentivizes fee-only planners to focus solely on providing unbiased financial advice. Additionally, fee-only planners are legally required to disclose all sources of compensation to their clients, ensuring complete transparency in their financial planning services. For individuals seeking objective financial guidance without the potential biases of commission-based compensation, working with a fee-only financial planner may be the best choice.

7. The importance of unbiased advice.

One of the key factors to consider when deciding whether to work with a fee-only financial planner or to opt for DIY financial planning is the importance of unbiased advice. In today’s world, there are plenty of financial products and services that can be marketed to consumers, and it can be difficult to know what’s truly in your best interest. When you work with a fee-only financial planner, you can rest assured that they have no hidden agenda in recommending certain products or services. They are compensated solely by the fees they charge, and therefore have no financial incentive to steer you towards any particular product or strategy. This can be especially important when it comes to making complex financial decisions, such as selecting investments or planning for retirement. With unbiased advice, you can trust that the recommendations you receive are based solely on your unique financial situation and goals.

8. The potential risks of DIY financial planning.

When it comes to financial planning, there are two options: working with a fee-only financial planner or doing it yourself (DIY). While DIY financial planning may seem like an attractive option at first glance, it’s important to consider the potential risks that come with it. One of the biggest risks is making mistakes due to lack of expertise or knowledge. You may miss important details or fail to consider all the options, which can lead to costly mistakes. Additionally, you may not have access to the same resources and tools that a financial planner does, such as specialized software and industry connections. This could put you at a disadvantage when it comes to making informed decisions and optimizing your financial plan. Finally, DIY financial planning can be time-consuming and may take you away from other important priorities in your life. Therefore, it’s important to weigh the potential risks and benefits of DIY financial planning before making a decision.

9. The benefits of expert advice.

If you’re unsure whether to work with a fee-only financial planner or DIY your financial planning, it’s important to consider the benefits of expert advice. A financial planner can offer personalized guidance and create a plan tailored to your specific financial goals and needs. They have expertise in areas such as investment strategies, retirement planning, tax planning, and risk management. With their knowledge and experience, they can help you make informed decisions and avoid costly mistakes. Additionally, a financial planner can provide ongoing support and adjust your plan as your situation changes over time. While DIY financial planning may seem like a cheaper option, the potential costs of making mistakes or not optimizing your financial plan can be much higher in the long run. Ultimately, it’s worth considering the benefits of working with a fee-only financial planner to ensure your financial success.

10. Choosing the best option for you.

When it comes to managing your finances, you have two main options: working with a fee-only financial planner or opting for a DIY approach. Both have their merits and drawbacks, and the best option for you will depend on your financial situation and personal preferences. If you are comfortable managing your own finances and have the time and knowledge to do so effectively, DIY financial planning may be the way to go. However, if you are busy or lack the expertise to handle complex financial matters, working with a fee-only financial planner may be the better option. Ultimately, the key is to carefully evaluate your needs and goals and choose the approach that will help you achieve them most effectively and efficiently.

Real-life examples and case studies

Case study #1: DIY Financial Planning

Mahesh is a recent college graduate who wants to start managing his finances but doesn’t have a lot of money to spare. He decides to take a DIY approach to financial planning and starts reading personal finance blogs, listening to podcasts, and watching online videos to develop her knowledge.

Mahesh likes the flexibility of managing his finances on his own, and enjoys having control over his money. However, he starts to feel overwhelmed by the amount of information out there and struggles to make sense of all the conflicting advice.

After a year of managing his finances on his own, Mahesh realizes that he needs more guidance and decides to work with a fee-only financial planner.

Case study #2: Fee-Only Financial Planning

Kamlesh and Neha are a married couple in their 40s who want to retire in the next 10 years. They have some savings and investments, but are unsure if they are on track to meet their retirement goals.

They decide to work with a fee-only financial planner who specializes in retirement planning. The planner performs a comprehensive analysis of their finances and helps them develop a retirement plan that aligns with their goals.

Kamlesh and Neha appreciate the expertise and guidance of their financial planner, and feel confident that they are on track to retire comfortably. They are happy to pay the fees for the planner’s services, knowing that it will ultimately save them money and stress in the long run.

Tips and Actionable Advice

1. Assess your knowledge and skills: Before deciding if DIY financial planning or working with a financial planner is right for you, take an honest assessment of your knowledge and skills in personal finance.

2. Determine your goals: Consider your short-term and long-term financial goals to determine the level of support and guidance you need.

3. Research financial planners: If you decide to work with a financial planner, research different providers to find one that aligns with your needs and goals.

4. Ask questions: When working with a financial planner, don’t be afraid to ask questions and make sure you understand their recommendations.

5. Stay involved: Even if you work with a financial planner, it’s important to stay involved in the decision-making process and maintain control over your finances.

In conclusion, deciding whether to work with a fee-only financial planner or opt for DIY financial planning ultimately depends on your individual financial situation, goals, and comfort level. If you feel confident in your own financial knowledge and have the time and discipline to manage your finances, DIY financial planning may be a suitable option. However, if you prefer to have an expert handle your finances or you have a complex financial situation, a fee-only financial planner may be the better choice. Regardless of your choice, the important thing is to stay informed and be proactive in managing your finances to achieve your long-term financial goals.

If you need help in deciding whether DIY is suitable to you or not, you may asses yourself by clicking here.

Pingback: 10 Essential Steps for Effective Goal Based Financial Planning

Pingback: 6 Signs, you "need" to do your financial planning even if you don't "want"

Pingback: Investment Planning: Strategies to Build Your Portfolio and Grow Your

Pingback: Goal Based Financial Planning in india

Pingback: What to expect from my services as Financial Planner ?

Pingback: What Financial Planning is and what it is not?